A business sale can look simple on paper: price, closing date, done.

Then the draft LOI shows a twist. Part of the price is contingent. Part is withheld. Part sits with an escrow agent. Suddenly, you are not just negotiating the number; you are negotiating when you get paid and what has to happen first.

If you are dealing with an earnout business sale or seeing escrow holdback business sale language in a draft, this guide will help you understand what these tools do, why they appear, and which terms matter most.

Table Of Contents

- Why These Terms Show Up In Small Business Deals

- Earnouts Explained: The Basics And The Real Risk

- Escrows And Holdbacks Explained: What They Protect And How

- Earnout Vs Escrow Vs Holdback: When Each Makes Sense

- Key Earnout Terms To Negotiate

- Key Escrow And Holdback Terms To Negotiate

- Common Disputes And How To Prevent Them

- Where These Terms Belong In Your LOI And Purchase Agreement

- FAQs

- Conclusion And Key Takeaway

Why These Terms Show Up In Small Business Deals

Earnouts, escrows, and holdbacks are all tools for the same underlying problem: the buyer and seller do not fully agree on risk.

Sometimes the risk is about future performance. Sometimes it is about past liabilities that might surface after closing. Sometimes it is about both.

Earnouts are commonly used to bridge valuation gaps, but they can also become a source of post-closing conflict if the metrics and control rules are unclear.

Escrows and holdbacks are common ways to fund post-closing obligations, such as indemnification claims and purchase price adjustments.

Practical point: these terms are not “extra boilerplate.” They can change the deal’s real value.

Earnouts Explained: The Basics And The Real Risk

An earnout is a purchase price mechanism in which a portion of the purchase price is paid later, contingent on the business meeting agreed-upon targets after closing.

Why Buyers Like Earnouts

- They reduce the risk of overpaying when future performance is uncertain.

- They can help close a valuation gap when the seller is confident about growth.

- They can keep a seller engaged during a transition period.

Why Sellers Should Be Cautious

In a small business, the buyer’s decisions after closing can materially affect whether targets are hit. That is why disputes often involve topics such as accounting methods, expense allocations, pricing changes, integration decisions, and the amount of “effort” the buyer must put into pursuing the earnout.

If you are the seller, you are taking on credit risk with the buyer and operational risk in how the business is run post-closing.

Escrows And Holdbacks Explained: What They Protect And How

Escrows and holdbacks are not the same thing, even though people use the words interchangeably.

A holdback is when the buyer withholds a portion of the price and pays it later, contingent on conditions being met.

An escrow is when a neutral third-party escrow agent holds that portion and releases it in accordance with the escrow agreement’s rules.

What Escrows And Holdbacks Usually Cover

- Indemnification claims for breaches of representations and warranties

- Specific known risks, like unresolved tax items, open litigation, or missing consents

- Purchase price adjustments, like working capital true-ups

Many deal term studies and practitioner guides describe general indemnification escrows around 10% of transaction value, with timing tied to survival periods, although the right number depends on the risk profile and deal size.

Practical point: sellers often focus on the purchase price and ignore how long money is trapped in escrow, and what the buyer must do to make a claim.

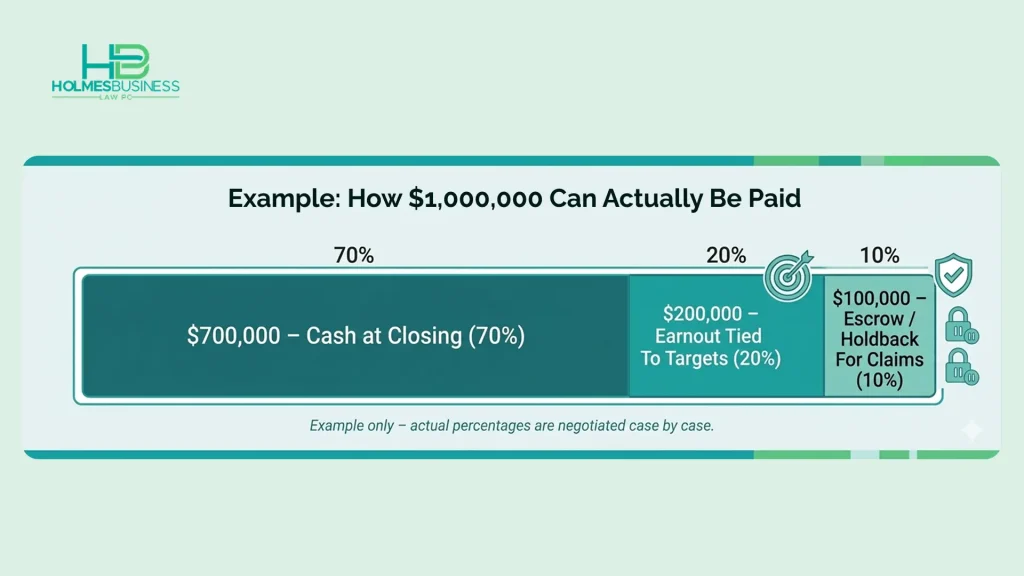

Earnout Vs Escrow Vs Holdback: When Each Makes Sense

Earnout Usually Fits When

- Buyer and seller disagree on the company’s growth potential, and performance is the real debate.

- The seller will stay involved, and the parties can define who controls decisions and reporting.

- The earnout metric can be measured cleanly.

Escrow Or Holdback Usually Fits When

- The risk is historical, meaning it already exists but may not show up until after closing.

- The buyer wants funded protection for indemnification or specific liabilities.

- The parties need a neutral process for releasing funds and resolving disputes (escrow), rather than relying on the buyer to pay later (holdback).

Many Deals Use A Combination

For example, part of the price may be contingent on performance (earnout) while a separate portion is set aside to cover indemnity claims (escrow/holdback). Your LOI should flag that early so it is not introduced late as a surprise.

Key Earnout Terms To Negotiate

If you only remember one thing about earnouts, remember this: the metric is not enough. You also need rules around control and measurement.

Earnout Metric And Definitions

Common metrics include revenue, gross profit, and EBITDA, but each can be manipulated, intentionally or unintentionally, if the definitions are vague.

Define, in plain language:

- Exactly what is being measured

- The accounting method and consistency requirements

- Any exclusions (one-time expenses, integration costs, owner perks removed, management fees, and so on)

Measurement Period And Payment Timing

Spell out:

- The earnout period length

- How often it is measured (monthly, quarterly, annually)

- When payment is due after the measurement date

- Whether partial achievement pays something, or it is all-or-nothing

Control, Efforts Standards, And Operating Covenants

A major earnout tension is this: the buyer owns the business, but the seller wants the buyer to run it in a way that gives the earnout a fair shot at success.

Many earnout disputes center on “efforts standards,” like commercially reasonable efforts, and on whether the buyer had discretion to change strategy.

If you are the seller, you may want:

- A defined efforts standard

- Limits on actions that would obviously depress the metric

- Reporting and access rights

If you are the buyer, you may want:

- Clear discretion to run the business

- Specific carve-outs for reasonable business decisions

- A tight, objective earnout formula to reduce subjective arguments

Reporting, Audit Rights, And Dispute Resolution

Include:

- What financial statements must the buyer provide, and when

- Whether the seller can inspect the underlying records

- A defined dispute process, often involving an independent accountant for accounting disputes

Acceleration And Exit Events

If the buyer later sells the business or shuts down the location, what happens to the earnout?

This should be addressed directly, because silence is where litigation grows.

Tax Treatment Awareness

Earnouts can create tax complexity for both sides, and the structure can affect the timing and character of income. Coordinate early with a CPA to ensure the contract terms align with the intended tax outcome.

Key Escrow And Holdback Terms To Negotiate

Amount And Duration

The right escrow amount is risk-based. Some market commentary suggests general indemnification escrows often cluster around a percentage of deal value, with durations aligned with reps and warranties survival periods, but there is no one-size-fits-all.

Negotiate:

- How much is held back

- How long has it been held

- Whether there are staged releases (for example, partial release at 6 months, final release at 12 months)

What Claims Can Be Paid From The Escrow

Be specific:

- Which indemnity claims qualify

- Whether certain items are carved out (taxes, payroll, fundamental reps, fraud)

- Whether defense costs can be paid from escrow

Claim Procedure And Deadlines

A clean escrow agreement answers:

- How the buyer must give notice of a claim

- What detail the notice include

- How the seller can object

- What happens if there is a dispute

- Whether funds stay frozen while a dispute is pending

Who Controls The Money

If it is a holdback, the buyer controls the release, which is why sellers often prefer escrow with a neutral agent.

Escrow Agent Terms

Do not ignore:

- Escrow agent fees, and who pays them

- Where the funds are held and whether interest accrues

- The exact release mechanics, including required signatures

Common Disputes And How To Prevent Them

Earnout Dispute Pattern

Seller says: You changed how the business is run, and the earnout became impossible.

Buyer says: We ran the business reasonably, and performance did not justify an extra payment.

This pattern is common enough that many advisors caution that earnouts can strain relationships if the contract is not tightly drafted.

Prevention checklist:

- Define the metric and accounting rules clearly

- Address integration and overhead allocation explicitly

- Include reporting and dispute procedures

- Align incentives if the seller will stay on

Escrow Or Holdback Dispute Pattern

The buyer makes a claim late with vague support, and the seller cannot get the money released.

The seller argues the claim is not valid, and the funds stay frozen.

Prevention checklist:

- Narrow what qualifies as a claim

- Require detailed notice and documentation

- Set firm timelines for objection and resolution

- Use an escrow agent and clear instructions when neutrality matters

Where These Terms Belong In Your LOI And Purchase Agreement

If these terms are likely, they should be flagged in the LOI. Otherwise, you risk a “deal re-trade” when lawyers draft the definitive agreement.

Your own LOI guidance already calls out earnouts and holdback/escrow as payment mechanics that should be identified early.

Why Choose Holmes Business Law For Earnouts, Escrows, And Holdbacks

Earnouts, escrows, and holdbacks can be useful tools in a small business sale, but they are also some of the most common sources of post-closing disputes. The difference usually comes down to drafting, clarity, and whether the documents match how the business actually operates.

Holmes Business Law helps buyers and sellers structure these terms so they are practical, enforceable, and less likely to turn into a fight later.

What Holmes Business Law can help you do:

- Translate deal concepts into clear contract language, including definitions for revenue, EBITDA, exclusions, and accounting methods, so the earnout calculation is not open to interpretation.

- Align the LOI and purchase agreement early, so that earnout, escrow, and holdback terms are not introduced late as a surprise that stalls closing.

- Build a fair escrow or holdback release process, including notice requirements, deadlines, supporting documentation standards, and a workable dispute process.

- Coordinate risk terms with the rest of the deal, including representations and warranties, indemnity caps, baskets, survival periods, and working capital adjustments.

- Reduce buyer and seller frustration by setting expectations up front on control, reporting, access rights, and the practical realities of running the business after closing.

If you are negotiating an earnout business sale or reviewing escrow holdback business sale language, you can explore services here:

Business Purchase Or Sale Service

Contact Holmes Business Law

FAQs

An earnout is a structure where part of the purchase price is paid after closing only if agreed performance targets are met.

It can be, but it adds risk. The seller is effectively financing part of the price, depending on future performance and the buyer’s post-closing decisions. The contract needs clear definitions, robust reporting, and well-defined dispute procedures.

A holdback is typically withheld and controlled by the buyer. An escrow is held by a neutral third-party escrow agent and released in accordance with the escrow agreement’s terms.

Often, the duration is tied to the duration of representations and warranties and the negotiated claim period. Some market sources cite common ranges, such as 12 to 24 months, for general items, but the right timeline depends on the specific risks in the deal.

At minimum: clear metric definitions, consistent accounting rules, reporting and access rights, an effort or discretion standard, and a dispute resolution process.

Yes. Earnouts address future performance uncertainty, while escrows/holdbacks often address historical liabilities and indemnification risk.

Conclusion And Key Takeaway

Earnouts, escrows, and holdbacks are not just “finance terms.” They are legal risk-allocation tools that can change who bears the downside after closing and whether the headline purchase price becomes actual dollars in your pocket.

If you are negotiating an earnout business sale or reviewing escrow holdback business sale language, the goal is clarity: clear definitions, clear timelines, and a clear process for resolving disagreements.

Key Takeaways:

- An earnout ties part of the price to future performance, so the metric, control rules, and reporting process matter as much as the number.

- Escrows and holdbacks protect buyers against post-closing claims, but sellers should negotiate the amount, duration, and a fair release process.

- Put these terms in the LOI early, so they are not re-traded late in drafting.

- The cleanest deals spell out notice requirements, deadlines, dispute resolution, and who controls the money.

- If the terms feel “standard,” that is exactly when they deserve a careful review, because small wording choices can shift thousands of dollars of risk.

If you want help structuring or negotiating these terms in your purchase agreement, you can start here: Contact Holmes Business Law