Buying a business can move fast, especially once the seller believes you are serious. That momentum is helpful, but it can also push buyers and sellers into misunderstandings that become expensive later.

A Letter of Intent is meant to slow things down in the right way.

It creates a clear, written starting point for the deal so both sides understand what is being purchased, how the price works, what needs to happen before closing, and what happens during due diligence. Well-written LOIs reduce wasted time, reduce disputes, and help keep negotiations focused.

If you are buying or selling a business in Pennsylvania, the LOI is often the first document that can shift leverage. It is worth getting it right.

Table Of Contents

- LOI Meaning In Business

- What Is A Letter Of Intent To Buy A Business?

- When An LOI Happens In The Business Purchase Process

- LOI Vs Purchase Agreement Vs Term Sheet

- Is A Letter Of Intent Legally Binding?

- What To Include In A Letter Of Intent For A Business Purchase

- Common LOI Pitfalls That Create Leverage Problems

- When To Involve A Business Lawyer

- FAQs

- Conclusion And Key Takeaway

Letter of Intent (LOI) Meaning In Business

LOI, meaning in business, refers to a Letter of Intent, a written document that outlines the key terms and major conditions of a proposed deal before the parties sign the final, definitive agreement.

LOIs are common in business transactions because they help both sides confirm the basic structure and expectations before investing heavily in due diligence, drafting, and negotiations.

What Is A Letter Of Intent To Buy A Business?

A letter of intent to buy a business is a preliminary agreement that summarizes the major deal terms a buyer and seller plan to negotiate into a final purchase agreement.

In a typical business purchase, an LOI helps answer practical questions early, such as:

- Are we doing an asset purchase or an ownership interest purchase?

- What is the purchase price, and how will it be paid?

- What is included in the sale and what is excluded?

- What information must the seller provide for due diligence?

- What conditions must be satisfied before closing?

An LOI is not the final contract. It is more like a roadmap that guides the next phase of the transaction.

When An LOI Happens In The Business Purchase Process

Most small business transactions follow a predictable sequence:

- Initial Discussions

The buyer and seller discuss a price range and the basic idea of the deal. - Confidentiality Agreement (NDA)

Before sensitive financial and operational information is shared, the parties often sign an NDA. This protects confidential information if the deal does not close. - Letter Of Intent

The buyer typically submits an LOI, and the parties negotiate it until a clear framework for moving forward is established. - Due Diligence

The buyer reviews financials, contracts, leases, intellectual property, employment issues, liabilities, and other risks. - Drafting The Purchase Agreement

The attorneys draft and negotiate the definitive purchase agreement and related closing documents. - Closing

If conditions are satisfied, the transaction closes, and the ownership transfer is completed.

LOI Vs Purchase Agreement Vs Term Sheet

These terms are often used interchangeably, but they are not the same.

Letter of intent (LOI): A preliminary document that summarizes key terms and process. It is often non-binding on the sale itself, although it may include binding clauses.

Purchase agreement: The definitive contract that governs the transaction. This document finalizes the legal and financial obligations of the buyer and the seller.

Term sheet: Often a shorter list of deal terms. In many transactions, a term sheet plays a similar role to an LOI, but the name varies by industry and deal size.

This distinction matters because people searching for “intent to purchase agreement” are often trying to determine which document actually binds them. In most cases, that commitment comes from the purchase agreement, not the LOI.

Is A Letter Of Intent Legally Binding?

In many business purchases, the LOI is generally non-binding on the ultimate sale, meaning either side can usually walk away before signing the purchase agreement.

That said, it is common for LOIs to include specific provisions that are intended to be binding, especially:

- Confidentiality (or reaffirming an NDA already signed)

- Exclusivity or no-shop provisions (the seller agrees not to solicit or negotiate with other buyers for a defined period)

- Sometimes, cost allocation, governing law, and procedural terms

Practical point: Do not treat an LOI as harmless paperwork. Even if the purchase itself is non-binding, certain clauses can create real obligations.

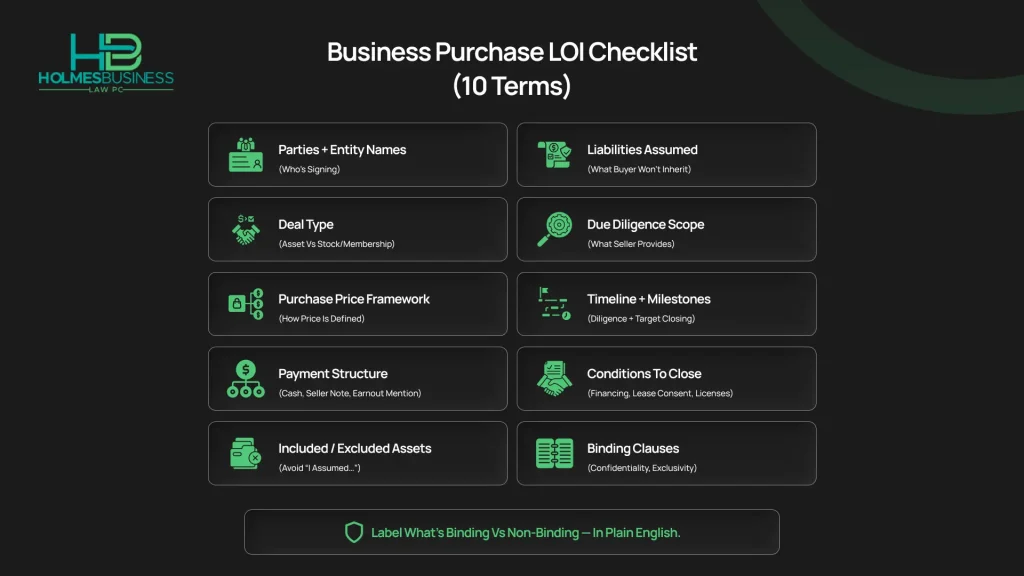

What To Include In A Letter Of Intent For A Business Purchase

A good LOI does two things at once: it captures the business deal in plain English, and it sets boundaries for what happens next (due diligence, drafting, and timelines). The goal isn’t to write the final contract; it’s to prevent misunderstandings and protect leverage before attorneys spend time (and money) building the definitive purchase agreement.

Below is a practical, buyer- and seller-friendly checklist you can use to strengthen this section without making it feel overly “legalese.”

1) The Parties + What’s Actually Being Sold

Start with clarity that removes ambiguity on day one:

- Legal names of the buyer and seller (and the entities involved)

- The business name and location(s)

- Deal type: asset purchase vs. stock/membership interest purchase

- A short description of the target (e.g., “operating assets of XYZ LLC, including customer relationships and IP”)

Why it matters: Deal structure drives taxes, liability exposure, and what must be transferred at closing.

2) Purchase Price + How It Will Be Paid

Don’t just state a number, state the mechanics:

- Purchase price (or purchase price range, if truly early-stage)

- Payment terms: cash at closing, seller financing, earnout, holdback/escrow, or a mix

- Any price adjustments (working capital/inventory adjustments, prorations, etc.)

- Whether the buyer is seeking third-party financing

Tip: If you anticipate seller financing or an earnout, mention it in the LOI so it isn’t a surprise later.

3) Included Assets + Excluded Items

This is where most “I thought that was included” disputes come from. Spell it out:

Commonly included items:

- Equipment, inventory, furniture/fixtures

- Website, domain(s), phone numbers, social accounts

- Customer lists, vendor relationships, goodwill

- Trademarks, trade names, other IP (as applicable)

Common excluded items:

- Cash on hand and certain bank accounts

- Owner’s personal assets/vehicles

- Specific receivables or liabilities that the seller keeps

Also, address at a high level:

- Accounts receivable / accounts payable treatment

- Key contracts that must be assigned (and whether consent is required)

4) Real Estate + Lease Issues (If Any)

If the business operates from a leased location, flag it early:

- Will the buyer assume/assign the lease, or sign a new lease?

- Is landlord consent required?

- Any known timing constraints (landlord review periods can slow closings)

This prevents a “great deal” from stalling because the location can’t legally transfer.

5) Liabilities + Risk Allocation (High-Level)

Even in asset deals, unclear language can create surprise exposure. The LOI should state:

- Whether the buyer will assume any liabilities (and which categories)

- Seller’s responsibility for pre-closing taxes, payroll, and filings

- Whether there will be an escrow/holdback for post-closing claims

- Any known red-flag issues already identified (pending litigation, tax debt, key contract risk)

You’re not drafting full indemnities here, just setting expectations.

6) Due Diligence Scope + Process

Make the diligence process feel structured (and fair) instead of open-ended:

- What the seller will provide (financials, tax returns, contracts, lease, employee info, permits, IP, etc.)

- Access rights: site visit, systems access, customer/vendor confirmations (and when allowed)

- A due diligence timeline (start date + target end date)

- Whether the buyer may speak with key employees, and under what conditions

Practical note: A timeline protects sellers from endless diligence and protects buyers from being “slow-walked.”

7) Conditions to Closing (Contingencies)

These protect both sides by making the path to closing realistic:

- Financing approval (if applicable)

- Satisfactory due diligence

- Landlord consent/lease assignment

- Transfer of licenses/permits

- Assignment of key contracts/vendor approvals

- Agreement on final purchase documents

This is where you prevent “we have a deal” from turning into “we have a misunderstanding.”

8) Exclusivity / No-Shop (If Used)

If the seller agrees to exclusivity, the LOI should be very clear:

- Whether exclusivity exists at all

- Length of exclusivity (specific dates)

- What is prohibited (soliciting, negotiating, accepting offers, etc)

- What happens if the seller breaches (at a minimum, termination rights)

Leverage point: Exclusivity can be valuable, but it must be time-limited and tied to a real diligence schedule.

9) Confidentiality + Publicity

Even if an NDA is already signed, the LOI should:

- Reference the NDA (or include confidentiality terms if none exist)

- Limit announcements/press releases without consent

- Address how information will be handled during diligence

10) Timing, Drafting Responsibility, and Deal Costs

Keep the deal moving by specifying who does what and when:

- Target signing date for the definitive agreement

- Target closing date (or range)

- Which side drafts the purchase agreement initially

- Whether each party pays its own legal/accounting fees

- Any deposits (and whether they’re refundable and under what conditions)

11) What’s Binding vs. Non-Binding (Make This Obvious)

This section prevents accidental legal obligations.

Most LOIs are non-binding on the sale, but they often include binding provisions such as:

- Confidentiality

- Exclusivity/no-shop

- Sometimes: expense allocation, governing law, dispute process

Best practice: Put a clear “Non-Binding / Binding” label on the relevant paragraphs to avoid confusion later.

Common LOI Pitfalls That Create Leverage Problems

An LOI should reduce uncertainty. Poorly drafted LOIs do the opposite.

Deposit Language That Is Too Risky

If a deposit is required, the LOI should clearly state:

- Whether it is refundable

- Who holds it

- What triggers a refund or forfeiture

This is a common practical issue that arises in template- and checklist-style LOI guidance.

Vague Due Diligence Rights

If diligence is described in broad terms without a timeline or deliverables, disputes start quickly. Buyers feel blocked. Sellers feel the buyer is fishing.

Exclusivity That Is Too Long Or Unclear

Exclusivity can be reasonable, but it must be time-limited and clear. Otherwise, the seller can lose opportunities while the buyer delays, or the buyer may believe the deal is protected when it is not.

Unclear Included Assets

A buyer might assume the website, phone number, contracts, and customer lists are part of the deal. A seller might assume those items are separate. The LOI should prevent those assumptions.

Binding Language That Does Not Match Intent

Some LOIs unintentionally read like a final agreement. Better drafting distinguishes between what is binding and what is not, avoiding confusion later.

When To Involve A Business Lawyer

A good rule is simple: involve counsel before you sign anything that affects leverage.

That includes:

- Broker forms that lock you into a process

- NDAs that shape what you can do with information

- LOIs that include deposits, exclusivity, or binding clauses

- Purchase agreements and closing documents

For buyers, legal review helps ensure the LOI includes protective contingencies, clarity around assets and liabilities, and a diligence process that fits your financing and timeline.

For sellers, legal review helps ensure the LOI does not give away leverage, does not create unintended binding commitments, and properly limits exclusivity.

How Holmes Law helps buyers and sellers use LOIs the right way

When a deal starts moving, the LOI is where many buyers and sellers accidentally give up leverage. A well-drafted LOI helps you avoid misunderstandings about price, assets, liabilities, and timing, and it keeps due diligence focused on what actually matters.

Holmes Law helps Pennsylvania business owners use LOIs as a practical tool, not a risky formality. That typically includes reviewing the proposed LOI before it is signed, tightening the terms that affect leverage, and clearly separating what is binding from what is not. We also help clients structure the deal to reflect real-world risks, whether that means clarifying which assets are included, addressing lease-transfer issues early, or building in realistic conditions from deal inception to closing.

If you are buying a business, we can help you protect your diligence rights, set financing-friendly timelines, and avoid hidden obligations that surface after closing. If you are selling, we can help you avoid overly broad diligence demands, long exclusivity periods, or language that creates unintended commitments.

FAQs

It is a document that outlines the main proposed terms of the transaction before the parties draft and sign the definitive purchase agreement.

Usually, the sale itself is non-binding, but certain provisions, such as confidentiality and exclusivity, are often written to be binding.

Most LOIs include the purchase price, deal structure, included and excluded assets, liabilities, due diligence timeline, closing conditions, and whether any provisions are binding.

The buyer typically conducts due diligence, and the attorneys draft and negotiate the definitive purchase agreement and closing documents.

Templates can help you understand common sections, but they cannot account for deal-specific risks like leases, hidden liabilities, licensing, or seller financing. Use templates as a reference point, not as a substitute for review.

Timing depends on diligence scope, financing, landlord approvals, and contract complexity. The LOI should set realistic diligence and closing targets that match your situation.

If your LOI includes exclusivity, deposits, or other binding provisions, legal review is strongly recommended, as these terms can affect leverage and risk early in the deal.

Conclusion

A Letter of Intent is more than a formality. It is the document that sets expectations, protects the diligence process, and prevents major misunderstandings before the purchase agreement is drafted. Done well, it saves time and reduces risk for both sides.

Key Takeaways:

- LOI meaning in business: a written summary of key deal terms before the final contract is signed.

- Most business purchase LOIs are non-binding on the sale, but confidentiality and exclusivity/no-shop clauses are often binding.

- The best LOIs clearly cover structure, price, included assets, liabilities, due diligence, contingencies, and timelines.

- If you want to avoid leverage problems, involve counsel before signing an LOI that includes deposits, exclusivity, or unclear asset and liability terms.